Ways to repay your mortgage

There are two styles of mortgage repayment – ‘repayment’ and ‘interest only’.

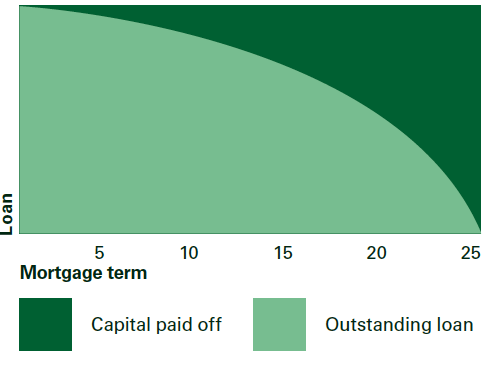

Repayment Mortgages

With a repayment mortgage, your monthly payments to the lender go towards reducing the amount you owe as well as paying the interest they charge. This means that each month you’re paying off a small part of your mortgage.

The advantages: You can see your mortgage getting smaller and provided you maintain the required payments, you also have the certainty your mortgage will be repaid at the end of the term.

The disadvantages: At the start, most of your payments go towards the interest on your mortgage. So in the early years, the amount you owe won’t reduce by very much.

Repayment Mortage

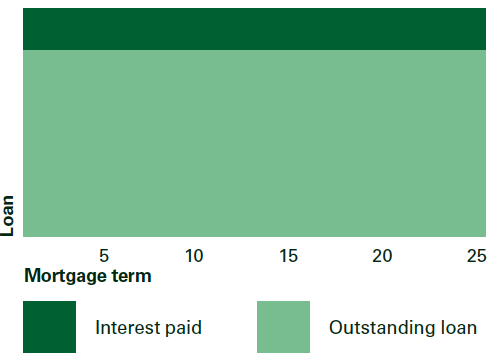

Interest only mortgages

These mortgages are now only offered with very strict criteria and are not available to everyone. With an interest only mortgage you only pay the interest charged on your loan, so you’re not actually reducing the loan itself. You’ll need to have a feasible repayment strategy in place to repay your loan at the end of the term, for example investments and/or savings plans. Lenders will want to see proof of these.

The advantages: If the savings or investment plan you choose performs well, then you could pay off your mortgage earlier compared to a repayment mortgage. At the full mortgage term there may be a lump sum available after the mortgage has been repaid.

The disadvantages: Very few investments or savings plans are guaranteed to repay your mortgage in full. If your savings or investment plan doesn’t cover the full amount, you’ll be responsible for paying the difference. Your mortgage lender can demand repayment, and they’ll charge you interest on any outstanding balance until it’s repaid.

You should discuss the risks with your adviser and make sure you’re comfortable with them.

Interest Only Mortage

Your home/property may be repossessed if you do not keep up repayments on your mortgage.

Fees and charges

Castle Mortgages offers and initial no obligation consultation. Following a successful mortgage application we will charge a fee based on the complexity of your application and how much work is required and this is only payable once we have found a solution for your needs. This will be discussed with you at your initial appointment. A typical fee charged will be £595.